Weekly Recap

It’s been a newsworthy week capped off by the news of the passing of Queen Elizabeth II.

For financial markets, traders contended with interest rate decisions from the RBA, BOC and the ECB, a new British Prime Minister confirmed, testimony from Fed chairman Powell and an OPEC+ production cut.

The RBA raised rates by 50 bps on Tuesday, kicking off a week of central bank meetings with hawkish forward guidance. With the country still battling rising inflation, the RBA signalled the likelihood of further rate hikes to come, a theme which would go on to dominate the week’s central bank commentary. Some concerns over the growth outlook in Australia saw a muted reaction initially but the Aussie went on to appreciate over the week as pro-risk flows helped lift sentiment.

The BOC delivered its fifth consecutive rate hike, this time by 75bps, taking rates up to 3.25%. Leading up to the meeting there had been some speculation that the BOC might announce a temporary pause in tightening on the back of this hike, or at least signal a likely pause in the near term. However, along with the hike, the BOC signalled that further increases are likely necessary as inflation remains elevated.

Finally, on Thursday we had the headline event of the week, the September ECB meeting. Lagarde and co did not disappoint. Along with the 75bps hike (the largest pan-European hike in over 50 years), the ECB signalled further hikes to come before year-end as it continues to battle soaring inflation in the Eurozone. With upward revisions to inflation forecasts, hawkish ECB expectations have seen the EUR rallying across the board into the end of the week.

With the focus elsewhere this week, USD softened from recent highs (despite hawkish Fed commentary over the week). While market pricing for a larger hike in September has become more concrete, the focus on EUR has seen USD bulls unloading for now, likely reflecting some positioning adjustment ahead of the upcoming FOMC meeting.

The weakness in USD across the week played into the hands of equities traders with most indices rebounding from initial lows on the week to trade back into the green. How sustained the move can be will very much depend on how the USD moves around the FOMC.

Commodities and oil prices also enjoyed a rebound this week, benefitting from a softer USD. Oil prices were additionally helped by news of a fresh OPEC+ production cut of 100k barrels per day from next month.

Coming Up This Week

- September BOE meeting

The BOE meeting will be the headline event this week with UK inflation at record levels in July, traders are looking for at least another 50bps worth of tightening. What will be of prime importance, is how the BOE addresses the new PM’s fiscal package unveiled this week given the warnings that the measures will drive inflation even higher still. With no new forecasts at this meeting, focus will be firmly on the comments made in the statement and Governor Bailey’s accompanying press conference.

- US CPI

The latest US CPI reading this week will be closely watched by markets as one of the two final pieces of tier-one data ahead of the September FOMC. While market pricing has moved firmly in favour of a larger 75bps hike, such an increase is still not fully priced in and there is two-way risk into this CPI reading on the back of a weaker print in July.

If CPI is seen moderating again, this might see pricing swing back in favour of a smaller 50bps hike by the Fed, pushing USD lower ahead of the meeting. Similarly, a fresh surge in CPI could confirm market expectations for a larger hike, sending the USD higher

- UK CPI

UK CPI will be closely watched ahead of the BOE meeting on Thursday. The market is firmly expecting a further hike from the central bank following record inflation in July. If CPI was seen rising further last month, this would push market forecasts towards a larger hike from the BOE, driving GBP higher. Given the backdrop, it would likely take a sharp downside surprise to dilute hawkish BOE expectations.

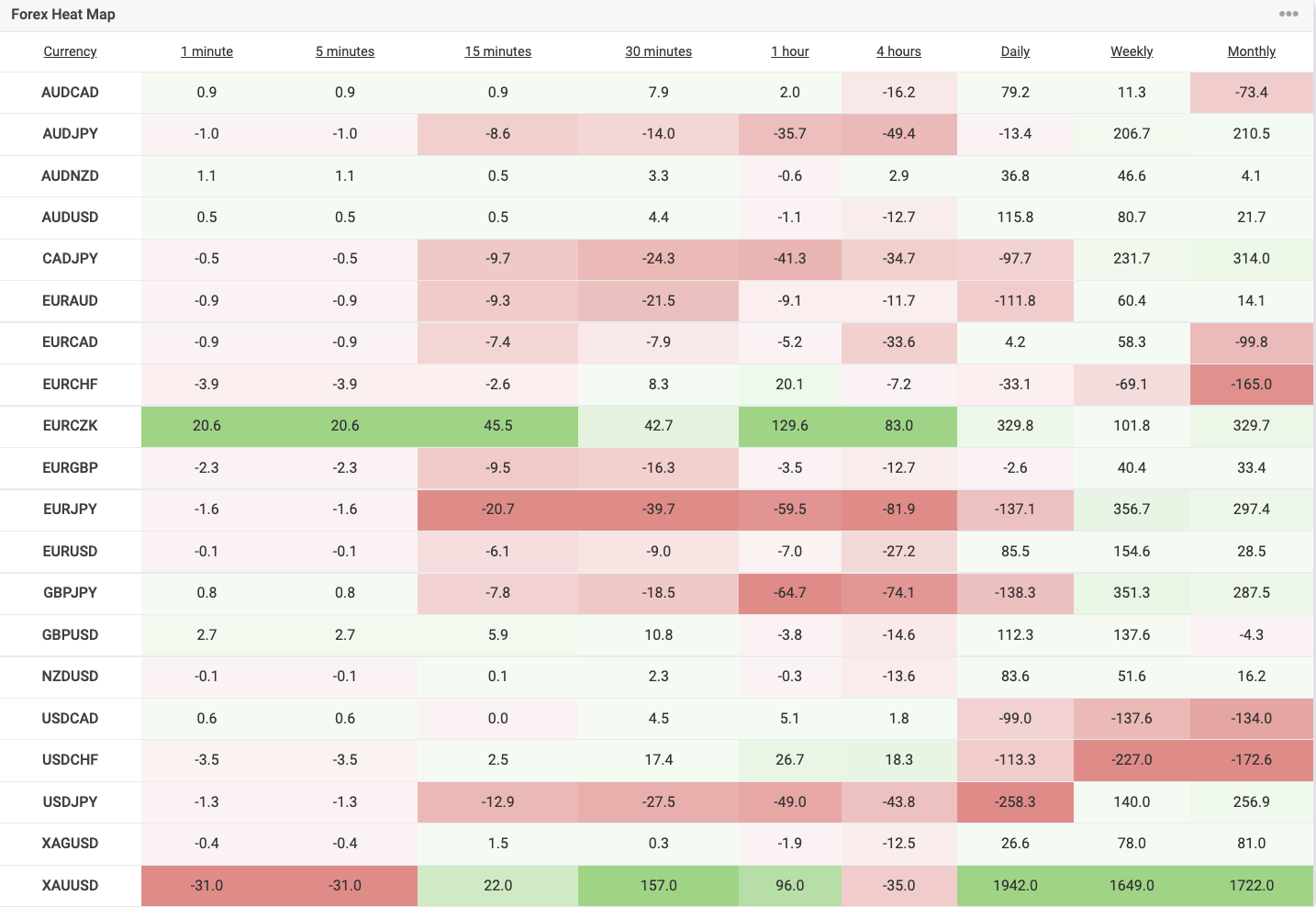

Forex Heat Map

Technical Analysis

Our favourite technical chart of the week – CADJPY

CADJPY has been rallying this year within a clear bullish channel. Price has now broken above the block of resistance which formed around the former 2022 highs, breaking out to fresh YTD highs.

The move has currently stalled at 109.70 resistance, yet while still within the channel the outlook remains bullish. Should the price correct lower from here, look for a retest of the 109.70 area to act as support for a fresh leg higher with only a breach below that level impacting this outlook.

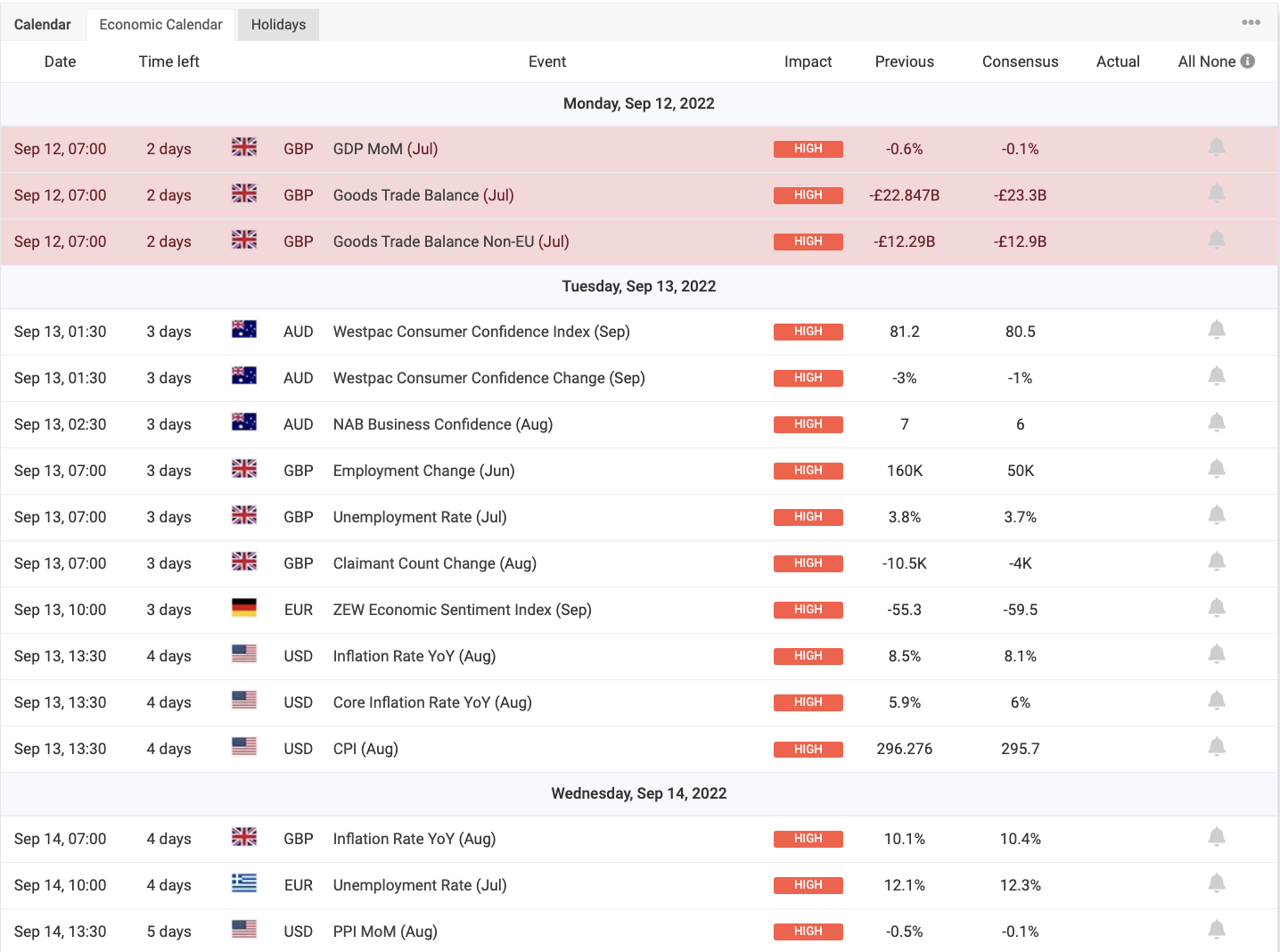

Economic Calendar

Plenty to keep an eye on this week data-wise, with the latest US and UK CPI and the September BOE meeting, among other key events and releases. See the calendar below for the full schedule.

Disclaimer: This article is not investment advice or an investment recommendation and should not be considered as such. The information above is not an invitation to trade and it does not guarantee or predict future performance. The investor is solely responsible for the risk of their decisions. The analysis and commentary presented do not include any consideration of your personal investment objectives, financial circumstances, or needs.