US Retail Sales & UK Inflation Data Due This Week

Weekly Recap

It’s been a highly volatile week for markets with the US dollar completing its longest weekly winning streak since January 2015!

Soaring inflation and hawkish Fed expectations continue to underpin the greenback. April CPI, whilst weaker than the heavy increase in March, came in above estimates. Later in the week we heard from Fed chairman Jerome Powell who warned markets that the Fed might not be able to avoid a hard landing in its efforts to bring inflation under control. Confirming the coming .5% hikes projected for June and July, Powell also signalled the possibility of larger .75% hikes if needs be.

The rally in USD saw equities markets and the broader risk complex come under heavy selling interest over the week. Equities and commodities tanked amidst rising US rates. The backdrop was then intensified by a severe rout in cryptocurrencies which saw market leader bitcoin cratering by 25% over the week. Excessive crypto losses fuelled the downside in equities as traders sought to fund crypto margin calls.

With risk aversion sweeping through markets over the week, the big winners in FX were USD and JPY, which both benefited from safe-haven in-flows. EUR saw some gains over the week but came under pressure as markets reacted with caution to ECB chief Lagarde signalling a potential July rate hike, sharpening the focus on eurozone growth concerns. In the UK, a slew of negative data saw the Pound heavily sold with preliminary Q1 GDP falling short of expectations, underscoring slowdown concerns.

Gold and silver ended the week lower, collapsing under the weight of a rampant US Dollar. Oil prices, meanwhile, were able to recover off initial lows on the week, recovering around 80% of Monday’s losses, as of writing. EU leaders continue to negotiate a proposed ban on Russian energy. However, with talks stalling, a full ban is now looking less likely with some sort of incremental phasing-out of Russian oil looking more likely. OPEC confirmed they would stick to gradual production hikes again this month, keeping oil prices supported.

Coming Up Next Week

- US Retail Sales

The next big US econ data is due this week with US retail sales due on Tuesday. Given recessionary fears taking hold in the US, this release will draw plenty of attention. With inflation still at excessive levels, interest rates having gone up and consumer confidence having tanked recently, risks of a material drop in retail sales are prevalent. Given the importance of this release for calculating overall GDP, a poor result will likely underscore fears of a coming slowdown in the US, putting further pressure on the Fed as it seeks to avoid a hard landing.

- UK CPI

UK inflation data on Wednesday will be closely watched by GBP traders. On the back of a slew of data misses last week, GBP sentiment has turned even more bearish near term. Traders will now be looking to see whether CPI moderated from the prior month’s high of 7% or if prices were still rising last month. A further uptick in inflation will no doubt heighten fears of a coming UK recession, putting greater pressure on the Pound as calls grow for the UK government to release an emergency “mini” summer budget to help support the economy.

- AUD Employment data

Aussie employment data on Thursday will be closely watched as the last tier one data of the week. Strength in the Aussie labour market has been the bedrock of RBA optimism over the last year. As the country continues to transition out of the pandemic, benefitting from re-opening, the RBA is now trying to fight the negative impact of soaring inflation. Any weakness in this data release will likely raise concerns over the health of the Australian economy as it also suffers the weight of a slowdown in China amidst the recent lockdowns there.

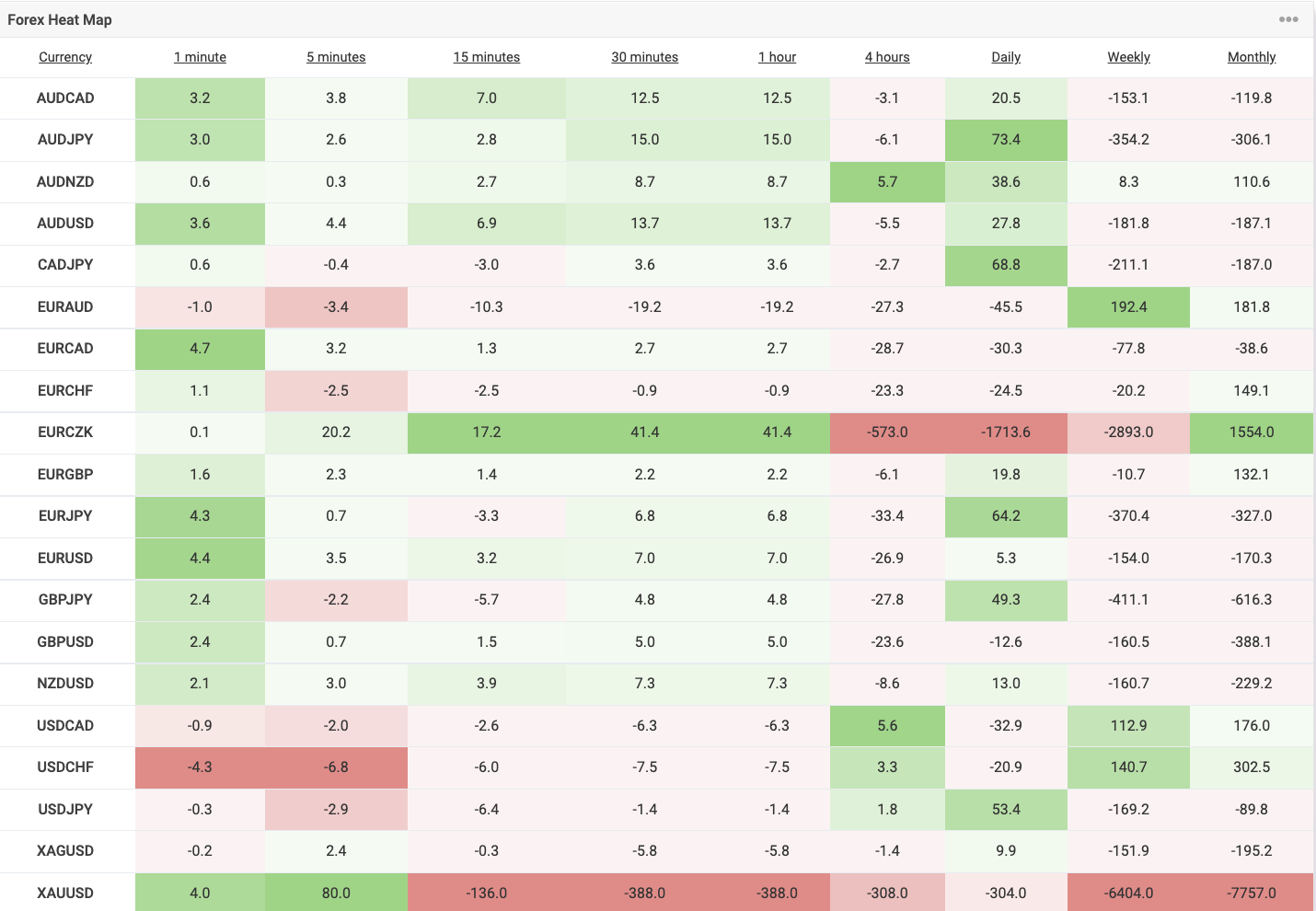

Forex Heat Map

Technical Analysis

Our favourite chart this week is AUDJPY

The reversal from 93.46 has seen the market correcting sharply lower. However, the broader bull trend remains intact while price holds within the bull channel. Looking ahead, the area around 85.98/86.0 represents strong support with the retest of broken prior highs coming in around the bull channel support level. While this area holds, the longer-term focus is on a continuation higher through 93.47/50. Only a break of the channel low will negate this view, raising risks of a move down toward 78.7 support.

Economic Calendar – High Impact

A very busy data sheet this week promises plenty of volatility with a slew of tier-one data including: CNY unemployment rate, GBP unemployment rate, CPI and retail sales, AUD RBA minutes and employment data, EUR employment data USD retail sales and many more, please see economic calendar below.

Disclaimer: This article is not investment advice or an investment recommendation and should not be considered as such. The information above is not an invitation to trade and it does not guarantee or predict future performance. The investor is solely responsible for the risk of their decisions. The analysis and commentary presented do not include any consideration of your personal investment objectives, financial circumstances, or needs.