Weekly Recap

It’s fair to say that compared with the action over previous weeks, it’s been a quieter session this week. Precious metals, equities and assets staged dependent on lower interest rates staged a relief rally on hopes that central banks were close to ending the monetary tightening cycle. These hopes were spurred on by the Reserve Bank of Australia which raised rates by a smaller amount than expected on the back of the Bank of England intervention last week.

The RBA caught traders offside with a smaller-than-expected rate hike this week. The market had been looking for a further 50bps hike and AUD was seen lower in response to the 35bps hike announced. The smaller hike seems to have somehow fed into the view that the Fed might be approaching its own rates pivot, despite guidance to the contrary. The RBNZ was then seen hiking by 50bps later in the week while signalling that further hikes are likely necessary.

The US Dollar initially sold off as gold and equities rallied but regained most of the losses by the end of the week. The greenback started the week trading lower in response to a weaker-than-forecast ISM manufacturing reading. However, into the second half of the week, the Dollar picked up as a better-than-forecast ISM services reading and ADP and NFP employment releases helped lift sentiment. Additionally, we’ve heard plenty of further hawkish commentary from Fed members this week placing the recent USD correction at odds with the Fed’s own guidance.

GBP recovered more of the losses suffered over the prior week in response to the controversial mini-budget announced by the UK government. However, GBP gains were surrendered in response to a speech from the new UK PM which went down very poorly with markets. The PM’s focus on growth, amidst growing concerns for UK households as winter approaches, saw GBP plunging lower again.

Finally, OPEC+ announced a fresh set of supply cuts. In a bid to help lift ailing oil prices, the group announced huge new cuts of 2 million barrels per day, the largest since COVID began. The move saw oil prices trading higher along with drawing plenty of pushback from the US government which criticised the group, warning against the economic impact of higher oil prices.

Coming Up This Week

- UK GDP M/M

The latest monthly UK GDP reading will draw plenty of attention this week amidst the recent market turmoil in GBP. At its last meeting, the BOE noted that the UK was likely already in recession and traders will now be looking to this data to confirm this view. Given the fears over the impact of the energy crisis this winter and with inflation still at record highs, any undershooting of market forecasts will likely see the GBP head sharply lower.

- US CPI

The latest US CPI release will undoubtedly be the headline event of the week. Given the recent re-emergence of speculation around a potential Fed pivot, September CPI has the potential to be highly market-moving. If inflation is seen holding at recent highs or surging to fresh highs, this will be firmly hawkish for the Fed, sending USD higher as the markets move to price in a larger hike in November. However, any surprise downside will no doubt give more weight to the idea of a Fed pivot, leading USD lower near-term.

- US Retail sales

Following the CPI print on Thursday, traders will then turn their focus to the retail sales release on Friday. Given recessionary fears in the US and the importance of retail sales in calculating overall GDP, Friday’s data will be used as a benchmark for overall economic activity and has the potential to cause plenty of volatility in USD and equities alike.

NOTE: US earnings season kicks off this week with banking giants JP Morgan and Citigroup among those reporting.

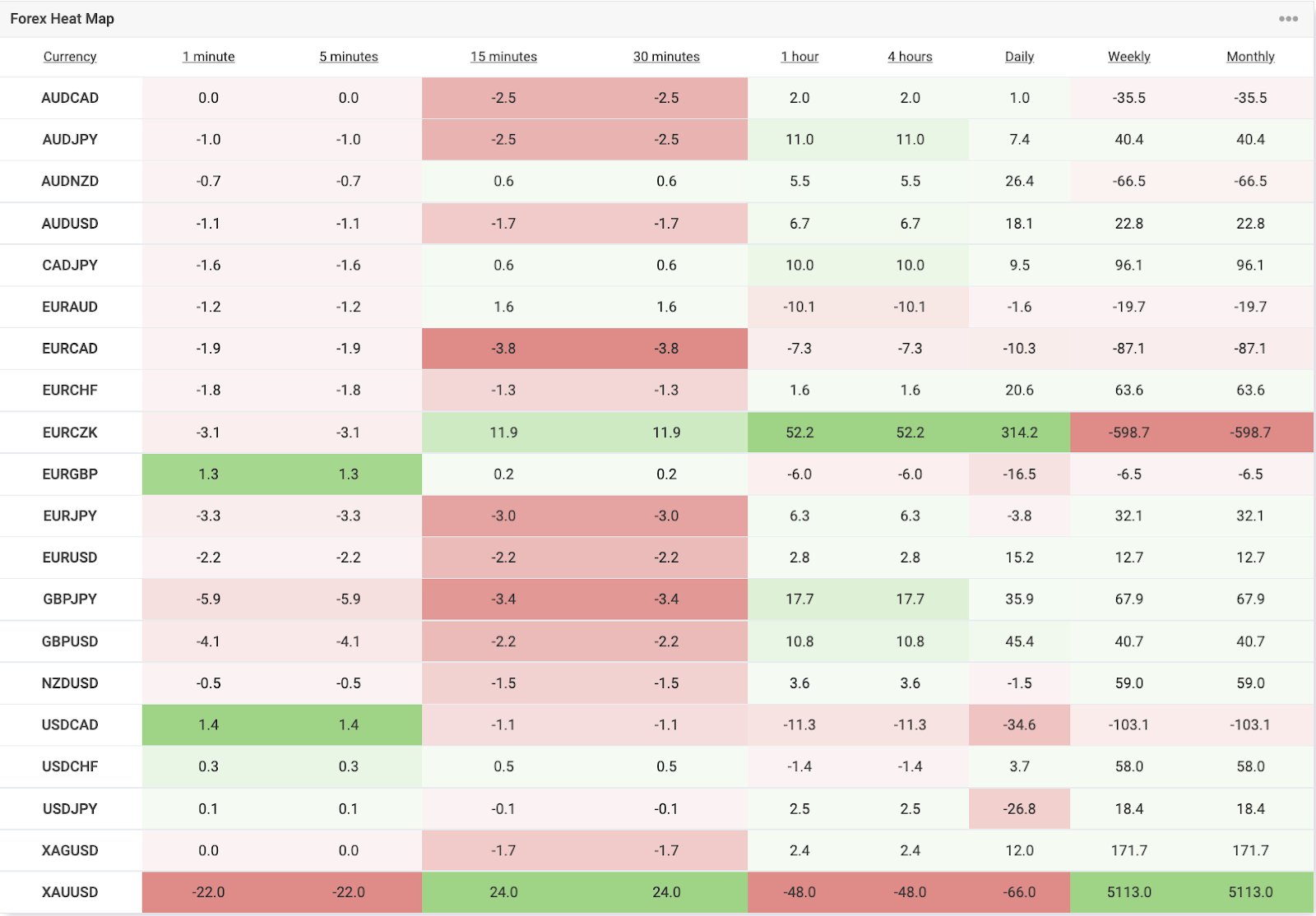

Forex Heat Map

Technical Analysis

Our favourite technical chart of the week – Copper Futures Weekly

Copper futures are sitting in an interesting position here. The latest test of the 3.2500 level has demand kicking in once again, raising the prospect of a double bottom forming here which would put the focus on a move up to the 3.7300 highs and above towards 4.0715. However, should the current consolidation resolve to the downside, a break of 3.2500 would put the focus on a move down to 2.2900.

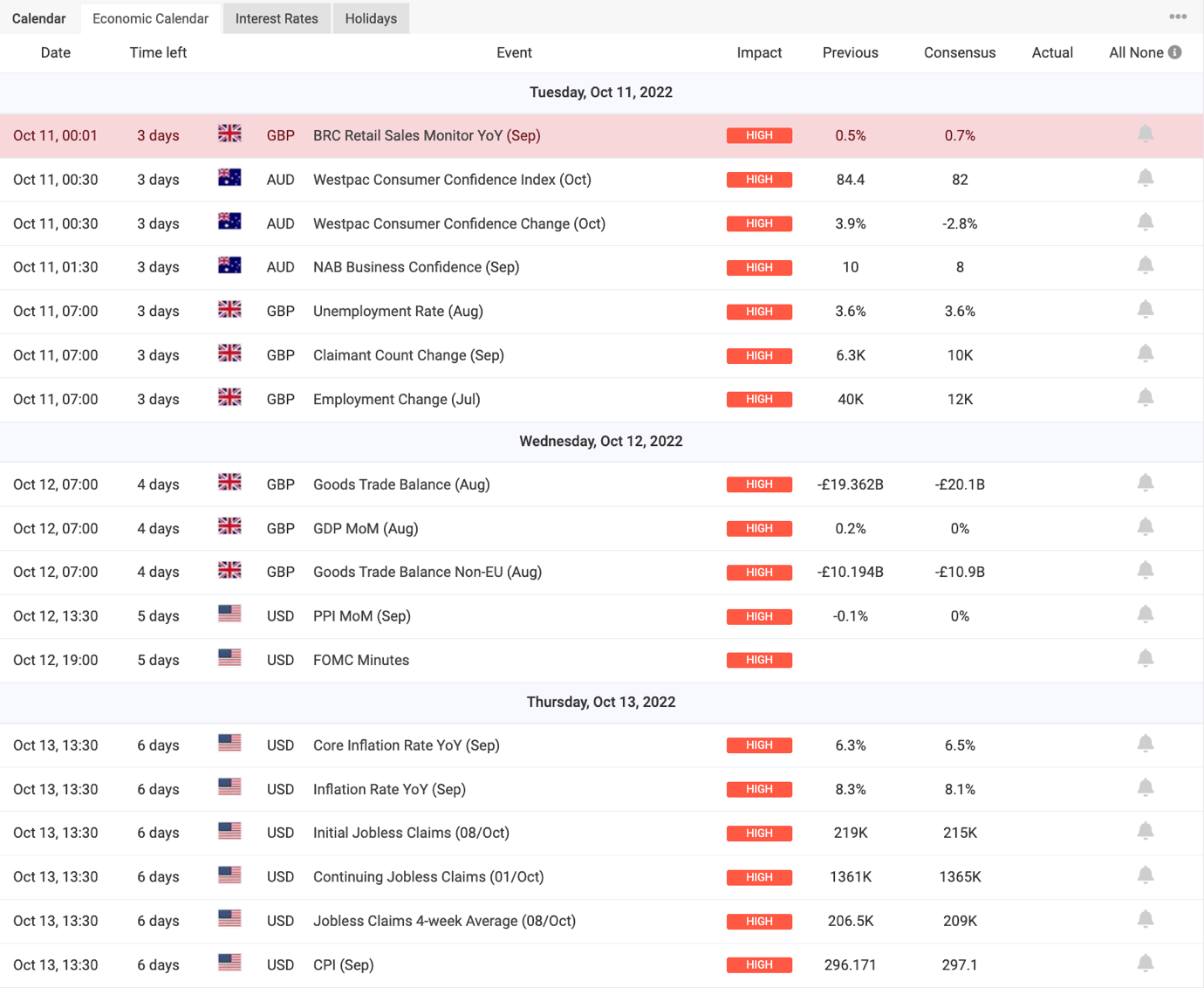

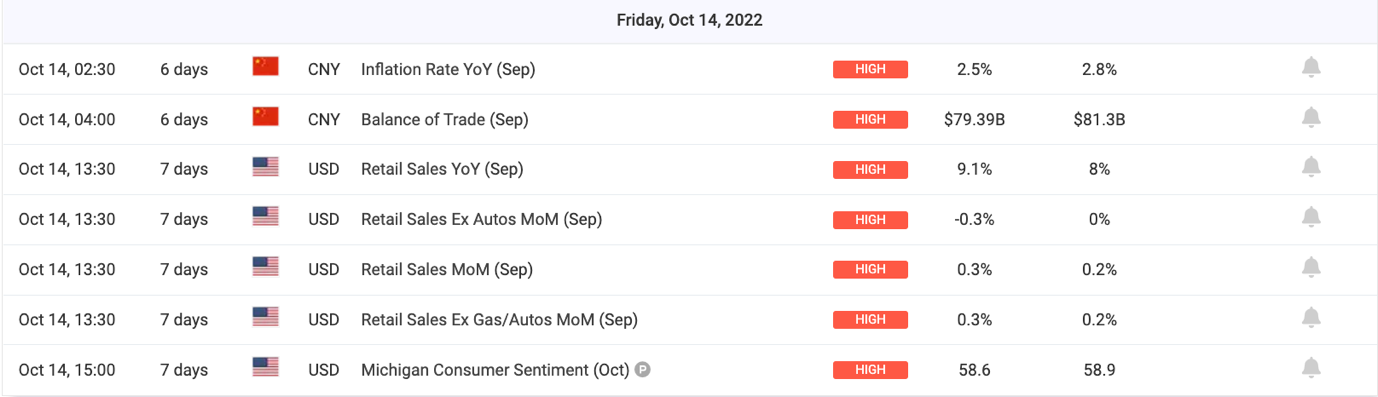

Economic Calendar

Plenty to keep an eye on this week data-wise, with the latest UK GDP, US CPI and US Retail sales data among other key events and releases. See the calendar below for the full schedule.

Disclaimer: This article is not investment advice or an investment recommendation and should not be considered as such. The information above is not an invitation to trade and it does not guarantee or predict future performance. The investor is solely responsible for the risk of their decisions. The analysis and commentary presented do not include any consideration of your personal investment objectives, financial circumstances, or needs.